The recent real estate commission lawsuits have shaken the industry. Many realtors feel the public perception of our value has taken a direct hit. I started this podcast because I was angry about that. But staying angry isn't productive. Action is.

Financial literacy is our best defense. So I invited Nancy Benet from Fix-It Accounting onto the REalizations Podcast. She is a Florida-based CPA who works with agents nationwide. She understands the feast-or-famine nature of our business. Having survived my own early financial mistakes and an IRS audit, I wanted Nancy to help you avoid learning those lessons the hard way.

Listen to the full episode:

Beyond the Commission Lawsuits: Why Financial Literacy is Our Best Defense

This is a complex, high-stakes business. It requires more than just opening doors. Nancy runs Fix-It Accounting, a firm dedicated to helping realtors build wealth, not just generate income. According to the National Association of Realtors member profile data, the median gross income for realtors fluctuates dramatically, proving that cash flow management isn't just a skill; it is a survival mechanism.

Nancy sees it every day. Agents make a big sale, buy a luxury car, and then starve for three months. That cycle stops today. To build a sustainable business, you first need a solid financial framework. A great first step is learning to build real connections in your community to generate steady referral business. I also recommend reading up on how to boost your real estate business with effective call centers to keep your pipeline full without burning out.

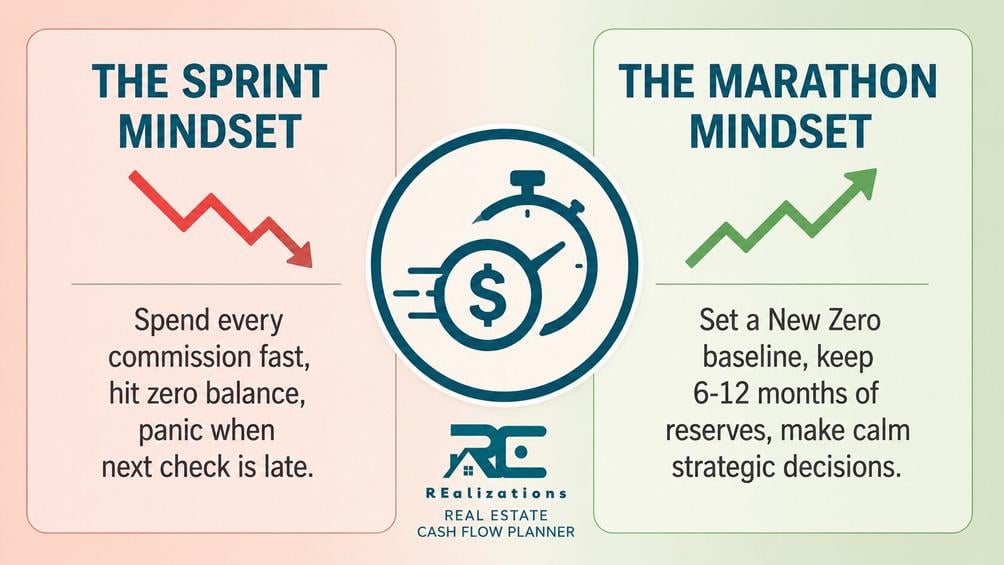

Cash Flow is King: Establishing Your "New Zero"

The biggest trap realtors fall into is looking for a quick fix. Business is a marathon, not a sprint. Nancy introduced a concept that completely shifted my perspective: the "New Zero."

Most agents spend down to a zero balance. You need to reset that baseline. Do not wait for a crisis to manage your money. The key to longevity is maintaining reserves.

"Commission-based is harder, and building a business takes time. I think people are just looking for a quick fix. So don't look at it that way. Look at it as more of a long-term obligation or long-term career. Business is a marathon. It is not a sprint by any stretch of the imagination. And it does go up and come down and go up and come down, and you have to prepare for those down times. And preparing would mean saving your money. Having a good investment strategy with your real estate."–

To survive, you need 6 to 12 months of expenses sitting in the bank. That is your new zero. If you have less than that, you are broke. Nancy says this seems daunting, but she built her reserve in just 90 days by changing her intention. She suggests running every expense through a dedicated business account to keep it clean, something she explains further when discussing the importance of good, clean financial statements for business owners.

If you want to understand how to structure your team for long-term success, check out how community-driven real estate builds long-term success on my blog.

Tax Strategies and the Power of the S-Corp

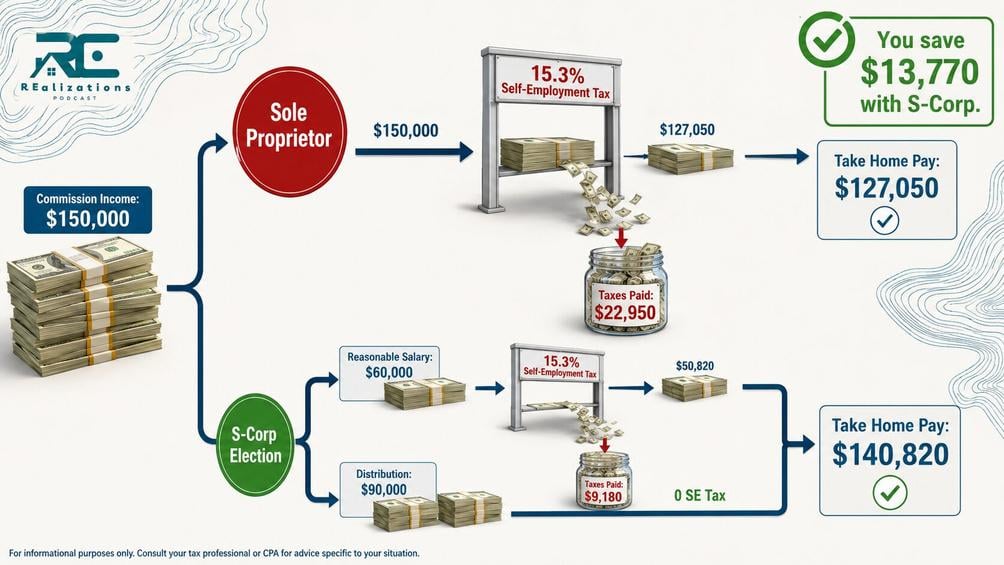

Many realtors get crushed by the 15.3% self-employment tax because they stay as sole proprietors too long. Nancy explains that an S-Corp tax benefit for realtors is the single most powerful tool to stop that leak.

You cannot just wake up one day and be an S-Corp. You need the structure first. Nancy advises forming an LLC. Once you are consistently profitable, you make the S election. You take a reasonable salary, subject to that 15.3% tax. The rest of your profit is not.

This saves you 15.3% on the remainder of your income. If that remainder is 100,000, you just saved over 15,000. It is a massive wealth accelerator.

"As a business owner, nobody's withholding funds for you. You have to pay both sides of Social Security and Medicare, the employer side and the employee side, and the federal income tax. And if you don't do something to minimize that, that can get really big, really fast because Social Security and Medicare is 15.3% of your total net income. It can be huge. Let's say you made a hundred thousand dollars; that's $15,300. If we make an S election, we take a reasonable salary. Reasonable is open to interpretation; it has to be reasonable for the IRS to accept it. But you take a reasonable salary that's subject to that 15.3%, and the rest of your ordinary income is not subject to self-employment tax. So you're saving 15.3% on the rest. And if that's a hundred thousand more or 200,000 more, that's a huge benefit to you."–

Nancy warns against missing obvious deductions. Many agents forget MLS fees, lockbox costs, and signs. Every dollar you deduct is a dollar the IRS doesn't tax. For a deeper dive on managing operations, read about the 3 keys to running a successful accounting practice on her firm's site.

The IRS publishes official guidelines on S corporation requirements that every realtor should review before making the election.

Maximizing the Real Estate Professional Tax Status

Nancy reminded me why we are in the best industry in the world. The tax code is written for us. If you qualify for Real Estate Professional Tax Status (REPS), your depreciation and paper losses can offset your ordinary income.

If you are spending 750 hours a year in real estate activities and it is your primary work, you are not just an agent. You are a real estate professional in the eyes of the IRS. This status allows you to take passive losses from rental properties and use them to wipe out your W-2 or commission income.

"If you're a real estate professional, investing in real estate is the best option for you. You could have real estate losses with your depreciation and all that offset your ordinary income, and you get to take all of that. It's beautiful. As a realtor, a real estate professional's status from a tax point of view is valuable. You could have real estate losses with your depreciation and all that, that offset your ordinary income, and you get to take all of that."–

This is a level of tax planning that TurboTax cannot handle. You can verify the specific hour requirements by reviewing IRS Publication 925, Passive Activity and At-Risk Rules, which details the 750-hour and more-than-50% tests for real estate professional status.

Using a real estate virtual assistant can help you log your hours to ensure you meet the REPS threshold without burning out. Also, consider navigating real estate investing across borders if you want to scale your portfolio strategically.

When to Fire TurboTax and Hire a Pro

Nancy's advice for newer agents was surprising: Don't over-engineer your business early on. You don't need a monthly retainer when you are starting. But you do need an annual gut check from a CPA who knows real estate.

A good CPA will ask the right questions. They ensure you aren't missing the deduction for your lockbox, your signs, or the cost-effective strategies like using call centers to nurture leads while you sleep. They will stop you from making devastating errors.

"I think in the beginning, when you have a new business, you really should contact a CPA, and you don't need a lot of services from that CPA. Don't let them talk you into the S election. Don't let them talk you into a monthly service package. You don't need that. You just need annual tax prep. What they can do is ask the right questions, make sure you're not missing deductions, and make recommendations for you and guide you along your way in business, because you need that. I think it's really important to have somebody who knows what they're doing. I failed at the first five businesses I had because I had no mentorship. And a CPA can provide some of that mentorship that you need."–

Nancy started her career with massive debt and no job. She knows the value of a dollar. She also knows that sometimes you need to resolve old tax debt before you can move forward. She has written about what an offer in compromise means and other tax terms to know. If you are underwater, learning about 3 tax resolution strategies the IRS offers is a tactical first step to financial freedom.

For those who want to be proactive, understanding IRS penalty abatement can save you thousands if you have already missed payments.

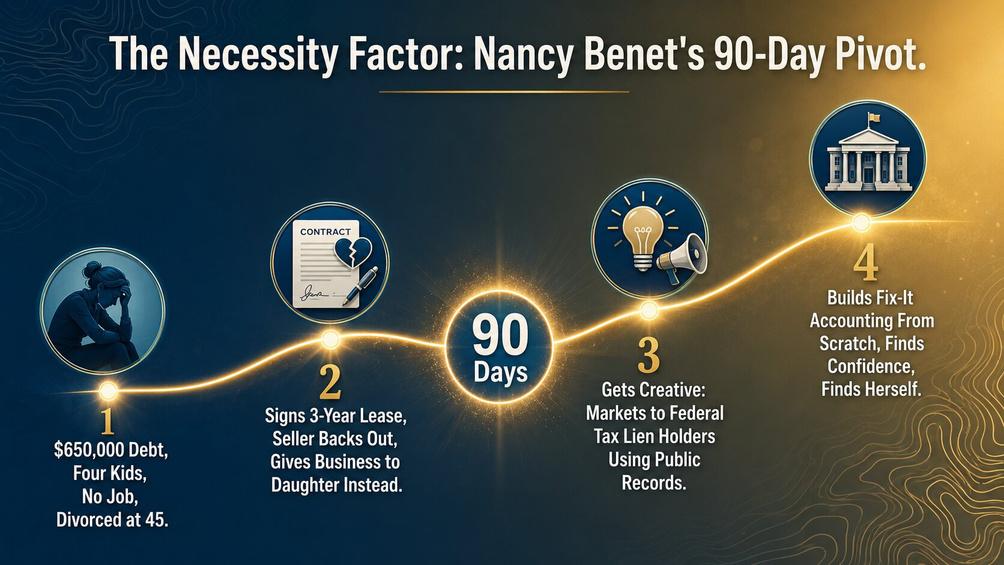

The "Necessity Factor": How to Turn a Crisis Into a Financial Fortress

What hit me hardest was Nancy's necessity mindset. She was $650,000 in debt with four kids and no job. Most realtors fail because they haven't felt that level of urgency yet.

The "Power of Intention" is not a fluffy concept. It is a tactical tool. Nancy built her "New Zero" in 90 days because she had to. Even after 28 years in this game, the moment you stop being creative is the moment you stop growing. If you are struggling, treat it as a call to action. Get creative. Look for opportunities in investing across borders or niche markets.

"I did what I did out of necessity, and I think that's the mother of invention. When you are locked into a corner, you don't have any choices. You just do what you have to do. I could have committed suicide or something, you can't when you have kids. And so that was a bleak time, but I would say that it's probably one of the most important times of my life. That formed who I am. And I found my confidence. I found my ability, I found myself through that process. And so don't be afraid to do hard things, I guess, is my message from that."–

Want to hear my entire conversation with Nancy Benet about S-Corp strategies, the "New Zero" cash flow plan, and how she climbed out of $650,000 in debt to build Fix-It Accounting? Listen to the full episode on the REalizations Podcast.

FAQ Section

When should a realtor switch to an S-Corp?

Nancy suggests making the S-Corp election once you are consistently profitable. It is a tool to minimize the 15.3% self-employment tax on your net income. Do not do it in year one, but have the LLC ready.

How much cash reserve is "safe" for a realtor?

The rule of thumb is 6 to 12 months of expenses. Having this "New Zero" allows you to weather health scares or market shifts without desperate decision-making. It turns a crisis into an inconvenience.

What are the biggest deductions realtors miss?

Beyond mileage, many forget MLS fees, desk fees, lockbox costs, and the signs they buy for listings. Also, remember your continuing education and professional development costs. Every dollar counts toward lowering your taxable income.

Build Your Financial Team

You cannot do this alone. Nancy has written about learning to say no so you can say yes to the right opportunities. She also offers controllership services for businesses that need daily financial management, not just yearly tax prep.

If you want to understand how to structure your operations further, read her post on everything you need to know about controllership services.

Apply as a Guest Speaker

Real estate is evolving. Capital is shifting. Markets are tightening. If you are actively working in the industry and solving real problems—whether in tax strategy, law, or investment—we want you on the show.

(510) 421-6818

(510) 421-6818

GET IN TOUCH

GET IN TOUCH

801 DELAWARE, BERKELEY CA 94710

801 DELAWARE, BERKELEY CA 94710