I've spent years in real estate, and one of the conversations that sticks with me most is a recent one I had on Realizations Podcast with Joel Kraut of Brrrr Loans.

Joel is a fix-and-flip lender who's been in the investment lending world for nearly three decades. What he shared about how this industry actually works, and what new flippers consistently get wrong, is exactly the kind of information I wish more investors had access to before they put down their first dollar.

So if you're thinking about flipping homes, this is your primer. And if you want to hear it straight from Joel himself, you can watch our full conversation below.

What Is a Fix and Flip Lender?

A fix and flip lender is a specialized financing source built specifically for real estate investors — not for people buying a primary residence. As Joel said plainly: "We're lending to investors."

These lenders provide home flipping loans to people who are buying distressed or undervalued properties, renovating them, and selling them for a profit.

Unlike a traditional bank, which is focused heavily on your income history and employment, a fix and flip lender is evaluating the deal:

-

The property

-

The renovation plan

-

And what the property will be worth after repairs.

Joel's company, Brrrr Loans, works with everyone from first-time investors buying their very first property to clients managing portfolios of 15,000 doors. The range is enormous.

But the mission is the same: Get investors the capital they need to execute.

How Home Flipping Loans Work

Home flipping loans are short-term financing tools for investors, not primary homebuyers.

“We specialize in lending across America to investors. We’re not doing primary residence homes. We’re lending to investors - investors on their journey from maybe their first property. And our largest client, once in a while will ask us to do something for them. They own 15,000 doors." — Joel Kraut, Brrrr Loans

Joel funds deals across the country — from single-family acquisitions to large-scale portfolios — and what distinguishes fix and flip lenders from traditional banks is both speed and focus.

They're evaluating the investment, not just the borrower.

Loan Structure

Fix and flip lenders structure their loans around the property and the project — not your W-2, which is the tax form your employers use to report your wages.

Approval is faster, around 10 days, and renovation costs can often be folded into the financing. That's a fundamentally different structure than anything a conventional bank offers to investors.

After Repair Value (ARV)

One of the core differences in how these loans are underwritten is that the lender looks at what the property will be worth after renovations are complete — not just what it's worth today.

This future-value approach is what makes home flipping loans work for investors who are buying below market, specifically to add value.

Here's how fix and flip financing compares to going the traditional bank route:

|

Feature |

Fix and Flip Lender |

Traditional Bank |

|

Approval Speed |

Fast (Around 10 days) |

|

|

Based on Future Value (ARV) |

Yes |

Rarely |

|

Renovation Funds Included |

Often yes |

Rarely |

|

Term Length |

Short-term (12–18 months) |

15–30 years |

|

Client Type |

Investors only |

Primary homebuyers |

The Rise of the Modern Fix and Flip Lender

Here's something most people don't know: the fix and flip lending industry as we understand it today barely existed before 2012.

Joel walked me through the history. Lenders like him were lumped under a category with a pretty ugly reputation. They were called hard money lenders — and the name carried a very specific connotation.

"We were these evil people, had cars with tinted windows, kind of roll by, roll the window down — you're supposed to make a payment or we took your property. That was sort of the connotation." — Joel Kraut, Brrrr Loans

Then, around 2012, something shifted. The market stabilized. Properties were still plentiful and relatively affordable.

And for the first time, the common people had access to a genuine opportunity: buy a distressed property, put some work into it, and sell it higher.

Flipping became a business. A real one. And the capital followed.

Joel described how early deals were stitched together by calling ten friends and collecting $30,000 each to fund a single $300,000 loan.

Now? Billions of dollars flow through Wall Street conduits into this space.

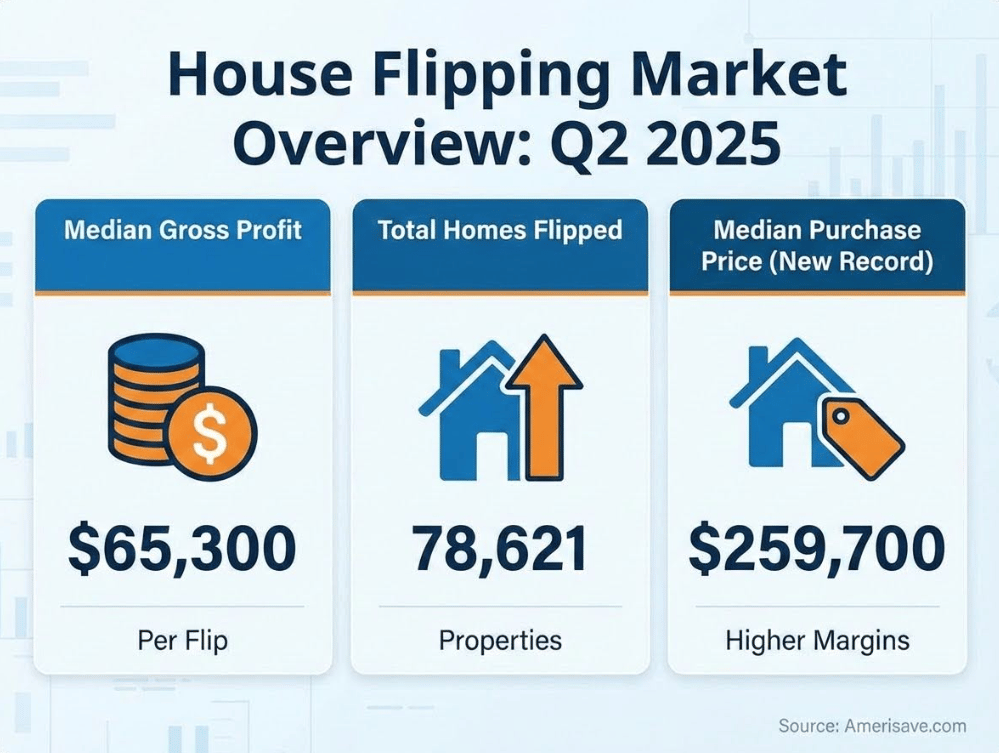

In Q2 of 2025:

-

House flipping generated a $65,300 median gross profit.

-

A total of 78,621 homes flipped

-

And the median purchase price for flipped properties hit a new $259,700 record, creating higher margins.

The industry exploded, and the sophistication of the lending infrastructure exploded with it.

"We went from really being these 'hard money lenders' to a niche... and we were fix and flip lenders." — Joel Kraut, Brrrr Loans

Lessons From 2008: Why Discipline Matters

Before you take out home rehab loans for flipping, you need to understand what happens when the lending industry loses its discipline. Joel lived through it, and so did I as a realtor navigating the aftermath.

There was one woman who worked at Glide Memorial Church, helping to house the homeless. She made six dollars an hour.

An unethical mortgage broker got hold of her and sold her four properties with zero down. She even received money out of the transactions.

Then the market turned.

-

Tenants couldn't pay rent.

-

All four properties started failing at once.

-

By the time I met her, she'd already been foreclosed on three of them and was fighting to hold onto the last one — not because it would help her credit (it was already ruined) but out of pride.

So I helped her short-sell that one last property.

And I know nothing ever happened to the mortgage broker who did that to her.

That story isn't ancient history. It's a warning about what happens when the incentives in lending get misaligned.

"You often see these problems arise when there's a misalignment between whoever's making a lot of the fee income and who really has the money. When that disconnect gets too big, there's an explosion." — Joel Kraut, Brrrr Loans

That explosion was 2008. And it's the reason today's fix and flip underwriting is fundamentally different: more disciplined, more investor-protective, and more accountable.

The pendulum swung hard in response, and not all of it was proportionate, but the core lesson held: discipline protects investors.

The Biggest Mistakes New Flippers Make

This is the part of my conversation with Joel that every new flipper needs to hear before they borrow a dollar.

|

Mistake |

What It Means |

|

Unrealistic Sell Timelines |

Expecting deals to close faster than the market realistically allows — then panicking when they don't |

|

Thin Margins |

Leaving too little room for mistakes, delays, or unexpected costs. |

|

Underestimating Insurance Costs |

Failing to account for how unpredictable or volatile expenses can be. |

Let me break these down, because each one is a deal-killer in its own way.

Unrealistic Sell Timelines

Two to four months on market used to be completely normal. Investors planned for it, priced for it, and weren't rattled by it. Somewhere along the way, expectations shifted — and now two months feels like a crisis. The market didn't change its fundamentals; flippers changed their assumptions. If your deal only works if you sell in two weeks, you don't have a deal — you have a gamble.

Before you borrow, build a sell timeline into your numbers that accounts for a slower market, not your best-case scenario. If the deal still works at four months, you're in a much safer position.

"It used to be two to four months was a normal sell cycle. Now, you get 2 months, and these people are in outright panic" — Joel Kraut, Brrrr Loans

Thin Margins

The math on a flip can look great on paper and collapse fast in real life. Run the numbers on a $1M deal with a $125K profit target and there's almost no room to absorb anything unexpected — a price reduction, an extended timeline, a surprise in demo.

Each setback chips away until you're at break even or worse. The fix is simple but uncomfortable: build your buffer in before you make the offer, not after.

Underestimating Insurance Costs

Insurance is one of the most volatile line items in a flip budget — and most investors don't find out until it's too late. Costs shift dramatically based on factors most people never think to check:

-

Location risk — coastal properties and fire zones carry significantly higher premiums

-

Coverage requirements — add-ons like law and ordinance coverage can spike a policy fast

-

Who you're talking to — one Texas deal came in at $18,000, jumped to $22,700 after required coverage was added, then came all the way back down to $1,370 by going to a different rep at the exact same company

Even two houses on the same block, with the same insurer, can come in at completely different numbers. I’ve seen quotes of $18,000 and $32,000 on near-identical properties.

With flipping home loans carrying real holding costs, every extra month is money out of your pocket — and an insurance bill you didn't plan for is one of the fastest ways to lose that margin. Get your quotes before you close, not after. And if the number looks wrong, push back.

“They don't realize what zone they're in... somebody's told them 'well it should cost about x.' and then it's really double xx or y and you spend a—we spent a lot of time going to some of our national providers and trying to fight that back down." — Joel Kraut, Brrrr Loans

Risk vs Reward in Today's Market

The honest truth about flipping right now? Some markets make sense. Some don't.

Joel pointed out that in high-cost markets — the Northeast, California — margins have thinned to the point where many investors are stepping back entirely. The opportunity has migrated toward lower-cost markets in the Southeast, where prices are low enough that investors can absorb some risk and still come out ahead. You're seeing real flows of investor capital moving from California, New York, and New Jersey into those areas, alongside money coming from the Middle East and parts of Asia.

He also made a point I think about a lot as a realtor. The long-term trajectory of real estate is upward. Joel said it simply:

"I don’t know when real estate prices will officially top out. They haven't topped out since the beginning of the Bible." — Joel Kraut, Brrrr Loans

I've seen this in my own life. My childhood home in Berkeley sold in 1968 for $67,000. It changed hands four years ago for $3.2 million. That's the long game. It doesn't go up every month but the trajectory over time is unmistakably upward.

What changes is where and when. Some investors focus on cash flow. Others care primarily about appreciation. Joel's point, and mine, is that neither strategy is wrong. They're just different. And you need to know which one fits your personality and your goals before you borrow a dollar.

What to Look for in a Fix and Flip Lender

Not all fix and flip lenders are built the same. Here's what Joel says actually matters when you're evaluating who to work with:

-

Transparent fees — no surprises at closing

-

Clear draw process — know upfront how renovation funds are released

-

Real market knowledge — a lender who understands your local market is protecting your capital, not just deploying it

-

Long-term client relationships — ask how many repeat borrowers they have

-

Human underwriting support — they should be someone who actually calls you back

"We don't use bots, we use people. Somebody will actually respond to you and call you. Not just text message you." — Joel Kraut, Brrrr Loans

Joel mentioned clients who've been with Brrrr Loans for 20-plus years. One client recently closed their 33rd loan with them. That's not a transactional relationship, but a partnership built on trust over time.

"Everybody's project is the single most important project they're working on. We try to do our best to recognize that." — Joel Kraut, Brrrr Loans

That mindset, treating every deal like it matters, regardless of size, is what separates a lender who's just moving capital from one who is actually on your team.

Who Should Use Home Loans for Flipping Houses?

The answer is: a lot of different people, for a lot of different reasons. But what matters most is knowing your own strategy first.

Joel works across the full spectrum of investors. Here's how to think about where you fit:

|

Investor Type |

Their Goal |

What to Look For |

|

First-time flippers |

Getting started with one acquisition |

Start small, learn the process |

|

Experienced investors |

Scaling an existing portfolio |

Speed and relationship matter most |

|

Out-of-state investors |

Targeting cash-flow markets in the Southeast or Midwest |

Need a lender with national reach |

|

Appreciation buyers |

High-demand coastal markets |

Discipline on margins is critical |

|

Foreign investors |

Bringing capital to the U.S. for stability |

Different risk profile, long-term view |

The home loans for house flipping that serve each of these investors look different. A first-timer in Florida is in a completely different position than a foreign investor parking capital in the Midwest for 20 years. A good lender knows that and structures accordingly.

What matters most is this: build a strategy that fits who you are and what you want. You're going to spend a lot of time on this. Make sure you actually want to be doing it.

FAQs About Fix and Flip Loans

Are hard money lenders the same as fix and flip lenders?

Not exactly — though the terms get used interchangeably. As Joel explained, "hard money lender" was the original label, with a real stigma attached. Fix and flip lenders evolved out of that space post-2008 with more structure, more institutional capital behind them, and a more investor-friendly approach. The product is more sophisticated, more transparent, and more mainstream than it was even 15 years ago.

How much down payment is required?

Given the short-term nature of fix and flip loans, down payment is typically between 10% to 25% of the price of the purchase.

Are home rehab loans for flipping risky?

All leverage carries risk. The bigger danger is going in underprepared — with thin margins, no buffer for extended time on market, or carrying costs you didn't account for. The risk isn't the loan itself. It's the plan behind the loan.

Can beginners qualify for home loans for house flipping?

Yes. Joel works with investors at every stage, including people buying their very first investment property. What matters is the deal quality and your ability to execute the renovation plan.

What credit score is required?

According to Loan Guys, a minimum credit score of 500 to 620 is required to apply for a fix-and-flip loan.

Ready to Flip?

Successful home flipping requires two things: the right property acquisition and the right capital structure. One without the other is how deals go sideways.

If you're looking for investment-ready properties in competitive markets, reach out to me directly. And if you're ready to structure smart, disciplined home flipping loans, reach out to Joel Kraut at Brrrr Loans — a seasoned fix and flip lender with nearly three decades of experience guiding investors through every kind of market cycle.

You can find Joel at Brrrr website, Instagram or LinkedIn.

This podcast is produced by the Icons of Real Estate - #1 Real Estate Podcast Network

Apply to Be a Guest on the REalizations Podcast

Real estate is evolving. Capital is shifting. Markets are tightening.

If you’re actively working in the industry and solving real problems, whether in construction, finance, brokerage, or development, we’d love to hear from you.

Apply to join the Realizations Podcast.