Most real estate investors hit the same wall: great deals, zero funding. Banks shut you down. Hard money lenders bleed you dry with points and fees. You're sitting on a goldmine property, and your money source just evaporated.

That's exactly where Jay Conner, private money expert and real estate investor, found himself in January 2009. He had two houses under contract with over $100,000 in potential profit when one phone call to his banker changed everything, and forced him to discover how private money lending could replace traditional bank financing entirely.

I brought Jay on to the Realizations Podcast to share exactly how he solved this crisis. Because understanding alternative funding strategies isn't just valuable for investors. Realtors who understand how their investor clients secure funding can position themselves as indispensable partners in the deal-making process.

"In January of 2009, I called up my banker. I had two houses under contract to buy, and the potential profit was over $100,000. I called to tell him about the funding that was required, and I learned over the telephone that my line of credit had been closed. Nobody told me about it."– Jay Conner

So Jay sat at his desk and asked himself one powerful question:

"I hung up the phone, sat at my desk, and asked myself a very powerful question: 'Jay, who do you know that can help fix your problem?”– Jay Conner

That crisis forced Jay to figure out how to raise private money for real estate — and in less than 90 days, he raised $2,150,000 from ordinary people in his network. Not banks. Not institutions. Regular folks with retirement accounts and investment capital looking for better returns than CDs paying less than 3%.

"Since that time, I've never missed out on a deal for not having the funding."– Jay Conner

Jay's completed over 500 flips using private money lending, and he's built a system that 47 private lenders trust with their capital.

Here's how he did it — and how you can do it too.

This conversation comes directly from my interview with Jay Conner on the Realizations podcast, where we unpacked his private money system step by step. You can watch the full episode here:

The “Birth” Of Jay Conner’s Private Money Lending Business

After his line of credit got cut, Jay needed a solution fast. His friend Jeff Blankenship mentioned something called "private money" and self-directed IRA companies. Jay had never heard of either.

"My friend said, 'Have you ever heard of private money?' I said, 'No.' He said, 'Have you ever heard about self-directed IRA companies where individuals can transfer retirement funds and loan that money out to real estate investors?' I said, 'I don't have a clue what you're talking about.”– Jay Conner

So Jay went to learn. Fast.

"The following month, February 2009, I went to my first real estate investing conference to learn about private money — and oh boy, did I learn about it."– Jay Conner

Here's what Jay did next — and this is the exact sequence you can follow:

Step 1 - He wrote out his opportunity

The interest rate he'd pay, how lenders could get their money back in an emergency, the length of the notes. Notice what's missing? No deal attached. He wasn't pitching a specific property. He was offering a standing opportunity.

"I came back home and the first thing I did was write out the opportunity I was going to offer people in my own network — the interest rate I would pay, how they could get their money back in case of emergency, and the length of the notes — without having any kind of a deal attached to it."– Jay Conner

Step 2 - He raised capital without asking for money

In less than 90 days, he raised $2,150,000 from ordinary people. Friends. Former colleagues. People in his network with retirement funds."In less than 90 days, I raised $2,150,000 in new funding from ordinary people — just ordinary people that had investment capital or retirement funds."

– Jay Conner

Step 3 - The "good news phone call"

Once he had committed lenders, he'd call them when he found a deal and put their money to work.

"Once I raised that money, I would call them up with what I call the 'good news phone call' and put their money to work — without ever pitching a deal."– Jay Conner

Notice the sequence: Educate first. Secure commitment. Then fund deals.

The Asset-Backed Lending Structure

Jay doesn't teach people to beg for money. He teaches them to offer a structured investment opportunity backed by real assets.

"I don't loan money. I teach other real estate investors how they raise their own private money from their own network."– Jay Conner

The most common question? "How do I start conversations about private money with potential lenders?"

"One of the most common questions I get is, 'How do I start conversations about private money?' So I created a script called the Curiosity Opener to help people start attracting private money."– Jay Conner

His entire framework shows real estate investors how to raise capital without asking for money — instead, you position yourself as an educator offering investment opportunities.

"I teach people how to raise private money without ever having to ask for money."– Jay Conner

The script isn't about your deal. It's about their opportunity. It positions you as someone offering a solution to their lazy money problem, not someone begging for capital.

|

Want to learn exactly how to start these conversations? Jay Conner created a script called the Curiosity Opener to help real estate investors start attracting private money without asking for it. Download the free PDF script here and start building your private lender network this week. |

Understanding After Repaired Value (ARV) and the 75% Rule

Want to know how Jay Conner has completed over 500 flips without a single private lender losing money? He never borrows more than 75% of the After Repaired Value (ARV).

Not the purchase price. The after repaired value.

"Another way we protect our private lenders is we give them a 25% equity cushion. We don't borrow more than 75% of the after repaired value of a single-family house."– Jay Conner

Here's how this plays out in real numbers:

The Deal:

|

Item |

Amount |

Why It Matters |

|

Purchase Price |

$100,000 |

What you pay to acquire the property |

|

Renovation Budget |

$40,000 |

Funds needed to improve the home |

|

After Repaired Value (ARV) |

$200,000 |

Projected value once renovations are complete |

Traditional Math: Most investors think "I'll borrow 75% of my $100,000 purchase" = $75,000. They're leaving money on the table and exposing their lenders to risk.

Jay's Math: 75% of $200,000 ARV = $150,000 maximum loan.

"If the after repaired value is $200,000, I'm not going to borrow more than $150,000. I didn't say 75% of the purchase price — I said 75% of the after repaired value."– Jay Conner

This creates a 25% equity cushion real estate strategy that protects the lender. Even if the market drops, even if the renovation runs over budget, even if you have to sell for less than ARV, your lender has a $50,000 buffer protecting their investment.

And here's the bonus: You're borrowing $150,000 on a property you're buying for $100,000. You walk away from closing with cash in hand to fund the renovation. No delayed draws. No begging for renovation funds.

Why This Matters for Your Lenders

Every single flip goes over budget. Jay's completed over 500, and not one came in exactly on the renovation estimate.

Your contractor finds rot in the subfloor. The electrical panel needs upgrading. The HVAC system dies mid-renovation.

Your profit margin shrinks. Maybe disappears entirely.

But your private lender? Still gets their 8% return. Still has their mortgage. Still has that 25% equity cushion protecting them.

This is why asset-backed lending works when partnerships fail. Your lender isn't your business partner hoping you make smart decisions. They're secured by an asset worth significantly more than what they loaned you.

How Realtors Support Jay Conner & Real Estate Funding

Jay Conner doesn't do this alone. He works with realtors who understand the game.

Chris Latham — 20 years in the business. Tracy Campbell — 15 years. They're listing agents. But they’re also providing the Comparative Market Analysis (CMA) that determines the After Repaired Value before Jay makes an offer.

Before Jay makes offers on any properties, his realtors send him a complete CMA with the after repaired value evaluation. They know what he's going to do to the house if he buys it — everything will look brand new and smell brand new — so they know how to pull the right comps.

Here's how I would explain it simply:

When buyers use an FHA 203K loan, they need a specialized appraiser who can value the property after renovations are complete. That appraiser provides the after repair value, and FHA determines lending amounts based on that future value — but the buyer can only put 3% down and must meet FHA's health and safety requirements.

Jay's system works the same way for determining ARV — except instead of FHA determining the loan amount, he's set his own rule: never more than 75% of ARV. And instead of specialized appraisers for every deal, he's built relationships with realtors who know his market intimately and can accurately comp the ARV.

The Exit Strategy: MLS and Lease-Purchase

The realtors also handle the exit strategy. Every renovated property gets listed on the Multiple Listing Service (MLS) with either Chris or Tracy.

Properties that don't need full renovation? Jay sells them directly via lease-purchase or rent-to-own, advertising on platforms like Facebook Marketplace. He helps buyers get ready for a mortgage while generating income from the property.

If you're a realtor reading this, here's your opportunity: Investors like Jay need reliable realtors who can provide accurate ARV comps and handle listings. Position yourself as the realtor who understands investor deals, and you'll have clients for life.

Comparison: Private Money Lending vs Traditional Bank Financing

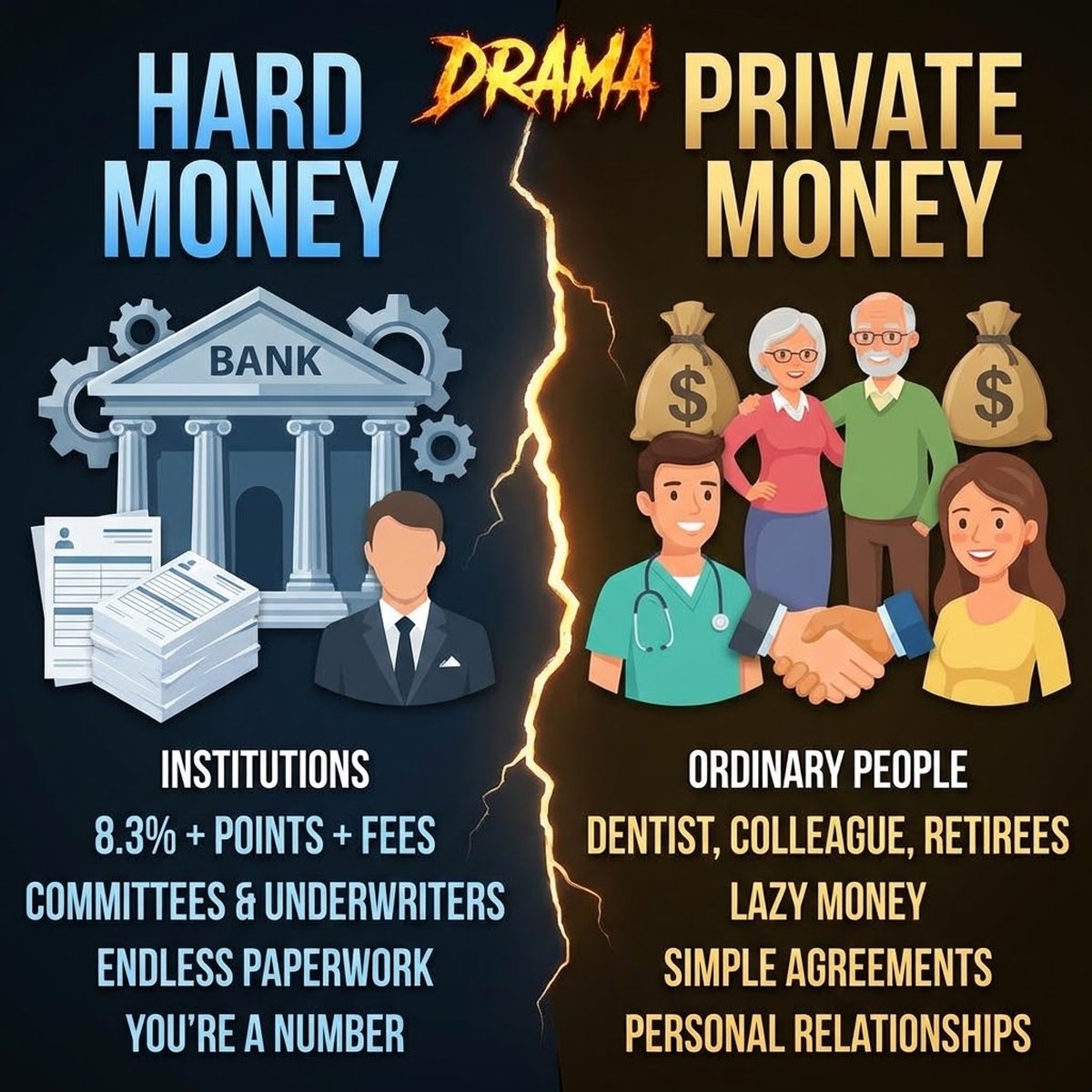

Before we get into Jay Conner's risk management strategy, let's kill the confusion about private lenders vs hard money lenders.

Private money is not hard money.

"Private money is not hard money. Hard money is institutional money. Private money is just ordinary people that have what I call lazy money — investment capital or retirement funds that's not working for them."– Jay Conner

Hard money comes from institutions. They charge 8.3% plus points plus origination fees. They have committees, underwriters, and endless paperwork. You're a number in their system.

Private money comes from ordinary people — the dentist down the street, your former colleague, the retired couple next door who have what Jay calls "lazy money" sitting in accounts earning nothing.

"Here we come along with a solution to get them a higher rate of return safely and securely than putting it in a CD earning less than 3% or putting it in the stock market and dealing with volatility."– Jay Conner

Let's run the same deal through both systems.

The Property:

|

Item |

Amount |

|

Purchase Price |

$100,000 |

|

Renovation Budget |

$40,000 |

|

After Repaired Value (ARV) |

$200,000 |

|

Needed Funding (75% of ARV) |

$150,000 |

Traditional Bank Route:

|

Category |

Details |

|

Interest Rate |

8.30% |

|

Points |

2 points = $3,000 |

|

Origination Fee |

$1,500 |

|

Approval Time |

30–45 days (if approved) |

|

Underwriting |

Credit score, income verification, DTI ratios, appraisal delays |

|

Total Upfront Cost |

$4,500 before renovations begin |

Private Money Route:

|

Category |

Details |

|

Interest Rate |

8% |

|

Points |

$0 |

|

Origination Fee |

$0 |

|

Approval Time |

As fast as you can call your lender |

|

Underwriting |

Relationship + asset-backed collateral |

|

Total Upfront Cost |

$0 |

"The local bank is charging 8.3% plus points and origination fees for a 30-year fixed investment mortgage. I'm paying my private lenders 8% — no points, no origination fees — because it's a direct one-on-one transaction."– Jay Conner

You're paying less interest than the bank charges. Your lender is earning more than they'd get anywhere else. And you're not hemorrhaging thousands in fees.

The local bank charges more. You pay less. Your lender earns more. Everyone wins.

Risk Management and Lender Protection

Here's why Jay Conner's 47 private lenders sleep well at night: everything is asset-backed debt.

Your private lenders aren't hoping your flip goes well. They're not crossing their fingers that you find a buyer. Their return isn't tied to your profit. They're the bank.

"Everything we do is asset-backed debt. These private lenders get their own promissory note and their own mortgage or deed of trust that collateralizes that note. Think of the private lender as the bank."– Jay Conner

If you don't pay them? They foreclose. They get the property.

"If I don't pay them, their legal recourse is foreclosure. They get the property."– Jay Conner

This isn't a partnership. It's not equity sharing. It's a loan secured by real estate — the same structure banks use, but with better terms for everyone involved.

Why Renovation Overruns Don't Sink Your Lenders

After doing over 500 flips, Jay knows the truth about renovations:

"After doing over 500 flips, none of them come in on budget as far as the renovation goes. But that's why the private lender's return is not tied to the profit whatsoever."– Jay Conner

Your contractor finds rot in the subfloor. The electrical panel needs upgrading. The HVAC system dies mid-renovation.

Your profit margin shrinks. Maybe disappears entirely.

But your private lender? Still gets their 8% return. Still has their mortgage. Still has that 25% equity cushion protecting them.

Diversification: Why 47 Lenders Instead of Two

"That's why we don't have just one or two private lenders. We've got 47. And not one of them had ever heard of private money until I put on my teacher hat and taught them."– Jay Conner

What happens when a lender needs their money back? Family emergency. Medical bills. Job loss. Life happens.

With 47 lenders, you're not scrambling to refinance your entire portfolio when one person needs out. You've got depth. Redundancy. Options.

And here's the thing: none of those 47 lenders had heard of private money until Jay taught them.

This is the entire system: Educate people in your network about private money lending. Show them the returns. Show them the security. Show them the asset-backed structure. Then let them decide.

You're not asking for money. You're offering an investment opportunity backed by real estate with better returns than they're getting anywhere else.

FAQs on How to Raise Private Money for Real Estate

What is Jay Conner’s Private Money lending training?

Jay Conner offers multiple training options for real estate investors who want to raise their own private money. His online courses teach the complete system — from identifying potential lenders in your network to structuring deals, creating promissory notes, and building long-term lender relationships. He also hosts the Private Money Conference three times a year (live events) and virtual Zoom events where he teaches the fundamentals of raising capital without asking for money. The Jay Conner real estate funding approach is built on education first, then capital raising. You can start with his free Curiosity Opener script at jayconner.com/scripts to learn his conversation framework.

What is the Jay Conner private money script?

The Jay Conner private money script, called the Curiosity Opener, is a conversation framework designed to help real estate investors start discussions about private money lending without directly asking people for money. Instead of pitching specific deals, the script helps you educate people in your network about private money as an investment opportunity — explaining the returns, the asset-backed security, and how it works. The goal is to position yourself as someone offering a solution (better returns than CDs or volatile stock markets) rather than someone asking for a favor. This shifts the dynamic from "Can you help me?" to "Would you like to learn about this opportunity?"

What is a private money lender for real estate investors?

A private money lender for real estate investors is an individual (not an institution) who loans their personal capital or retirement funds directly to an investor to fund real estate deals. These lenders receive a promissory note and a mortgage or deed of trust that secures their loan against the property — the same structure a bank uses. Private lenders typically earn fixed interest rates (often 6-10%) regardless of whether the investor's flip is profitable. Their return isn't tied to the deal's success; it's secured by the asset itself. If the investor doesn't pay, the lender's legal recourse is foreclosure. Private lenders are often ordinary people with "lazy money" in retirement accounts, CDs, or savings accounts looking for better returns than traditional investments offer.

What is the difference between private lenders vs hard money lenders?

Private lenders are individuals using their own capital or retirement funds to make direct loans to real estate investors. Hard money lenders are institutions or companies that pool investor capital and operate like traditional lenders with committees, underwriting processes, and standardized terms. The key differences: Private money typically offers better rates (8% vs 8.3%+), no points, no origination fees, faster approval (based on relationships and asset value rather than credit scores), and direct one-on-one transactions. Hard money charges higher rates, adds points (typically 2-4%), requires origination fees, and treats you like a number in their system. Private money relationships are personal and flexible. Hard money is transactional and rigid. Both are asset-backed, but private money is almost always cheaper and faster for investors with good deals and strong relationships.

Is private money lending legal?

Yes, private money lending is completely legal when structured properly. Private individuals can loan money secured by real estate using promissory notes and mortgages or deeds of trust — the same legal instruments banks use. Many private lenders use self-directed IRA companies to transfer retirement funds into accounts that can make these loans, with the interest earned being either tax-deferred or tax-free depending on the account type. However, private money lending must comply with state and federal lending laws, securities regulations, and usury laws (maximum interest rates). It's crucial to work with a real estate attorney who understands private lending to ensure your documents and structure are legally sound. The lending itself is legal; the structure and documentation must be done correctly.

How to Raise Private Money for Real Estate: Your Next Steps

Jay Conner proved something powerful in 2009: you don't need banks to fund deals. You need a system, education, and relationships.

The Jay Conner system for how to raise private money for real estate comes down to this:

-

Stop asking for money — Start offering an investment opportunity

-

Use asset-backed lending — Protect your lenders with promissory notes and mortgages

-

Never borrow more than 75% of ARV — Give lenders a 25% equity cushion

-

Educate before you raise — Teach people what private money is before presenting your opportunity

-

Build depth — Don't rely on one or two lenders; build a network of 10, 20, 47 lenders

-

Use the Curiosity Opener script — Start conversations that attract capital instead of begging for it

Since January 2009, Jay has never missed a deal for lack of funding. He's completed over 500 flips using private money. His 47 lenders trust him because the system protects them first.

You can build the same system.

Start here: Download Jay Conner's free Curiosity Opener Script and learn the exact conversation framework that attracts private money without asking for it. Then explore his Private Money Academy training to build your complete private lender network.

Stop waiting for banks. Start building your private money network today.

This podcast is produced by the Icons of Real Estate - #1 Real Estate Podcast Network.

Apply to Be a Guest on the REalizations Podcast

If you work in real estate, as a builder, investor, lender, agent, developer, or operator, and have insight worth sharing…

Let’s bring your story to the table.

Apply to be featured on the Realizations Podcast.